5 Quantile Regression in R

Author: Lan Wang and Ruosha Li

5.1 Goals

- Fit a quantile regression model in R.

- Test the significance of regression coefficients

- Creat and plot pointwise confidence intervals

5.2 R Package quantreg

- R package quantreg (developed and maintained by Dr. Koenker).

- Documentation: https://cran.r-project.org/web/packages/quantreg/quantreg.pdf

- Type the following in R for installation:

install.packages("quantreg")- Then, load the package by typing:

library(quantreg)

## Loading required package: SparseM

##

## Attaching package: 'SparseM'

## The following object is masked from 'package:base':

##

## backsolve5.3 Fitting linear quantile regression in R

rq(formula,tau,data,method,...)- method=“br” (default): simplex method. Efficient for problems with modest sample size (up to several thousands).

- method=“fn”: Frisch-Newton interior point method; more efficient than simplex for larger sample sizes;

- method=“pfn”: Frisch-Newton with pre-processing (suitable when n is very large).

5.4 Example 1: Fit quantile regression at one quantile level

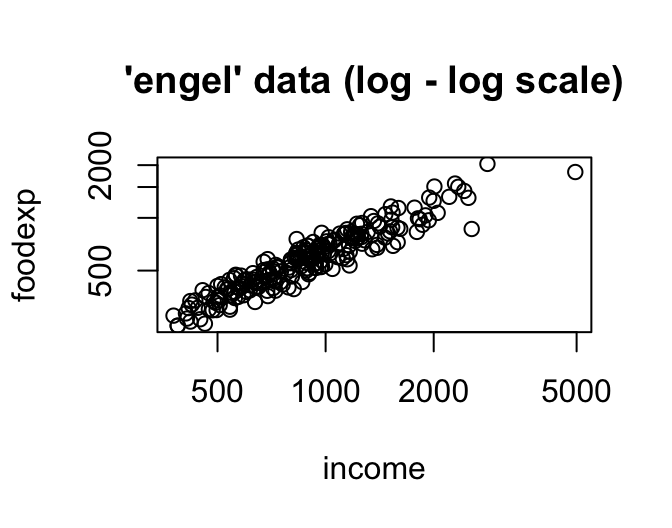

-Engel food expenditure data used in Koenker and Bassett(1982).

-This is a regression data set consisting of 235 observations on income and expenditure on food for Belgian working class households.

- income: annual household income in Belgian francs

- foodexp: annual household food expenditure

data(engel)

plot(engel, log = "xy", main = "'engel' data (log - log scale)")

f1<-rq(log10(foodexp) ~ log10(income), tau=0.5, data=engel)

f1

## Call:

## rq(formula = log10(foodexp) ~ log10(income), tau = 0.5, data = engel)

##

## Coefficients:

## (Intercept) log10(income)

## 0.1817 0.8766

##

## Degrees of freedom: 235 total; 233 residual5.5 Example 2: Fit quantile regression at multiple quantile levels simultaneously

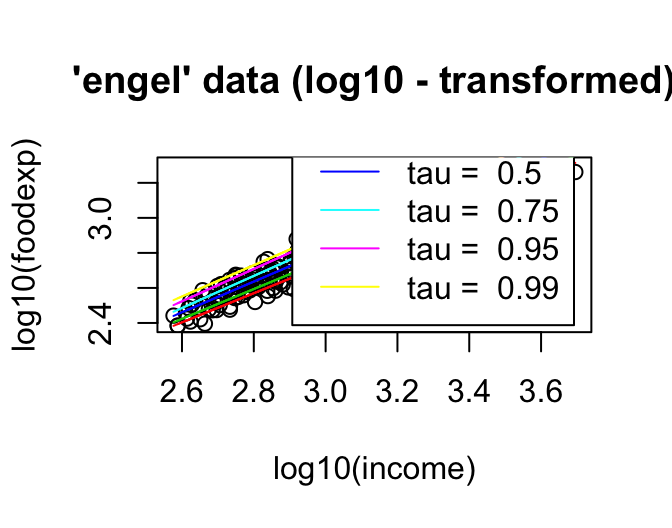

plot(log10(foodexp) ~ log10(income), data = engel, main = "'engel' data (log10 - transformed)")

taus <- c(.15, .25, .50, .75, .95, .99)

rqs <- as.list(taus)

for(i in seq(along = taus))

{ rqs[[i]] <- rq(log10(foodexp) ~ log10(income), tau = taus[i], data = engel)

lines(log10(engel$income), fitted(rqs[[i]]), col = i+1) }

legend("bottomright", paste("tau = ", taus), inset = .04, col = 2:(length(taus)+1), lty=1)

5.6 Inference on linear quantile regression in R

summary.rq(fit.obj,{\tblue{se=" "}},...)- se=“rank”: provides CI by inverting a rank score test.

- se=“nid”: estimation of the asymptotic variance assuming non i.i.d. errors (through sparsity estimation).

- se=“iid”: assumes i.i.d. errors in variance estimation.

- se=“ker”: variance estimated using a kernel estimate (Powell Sandwich).

5.7 Resampling methods for inference on quantile regression

summary.rq(fit.obj,{\tblue{se="boot"}},bsmethod="")- bsmethod=“xy”: xy-paired bootstrap.

- bsmethod=“pwy”: perturbing the estimating equation (Parzen, 1994)

- bsmethod=“mcmb”: Markov chain marginal boostrap (He and Hu, 2002), computationally efficient for large n and p.

- bsmethod=“wxy”: generalized bootstrap with unit exponential weights.

- bsmethod=“wild”: wild bootstrap (Feng et al., 2011).

f1<-rq(log10(foodexp) ~ log10(income), tau=0.5, data=engel)

summary.rq(f1, se="boot", bsmethod="xy", R=1000)

##

## Call: rq(formula = log10(foodexp) ~ log10(income), tau = 0.5, data = engel)

##

## tau: [1] 0.5

##

## Coefficients:

## Value Std. Error t value Pr(>|t|)

## (Intercept) 0.18168 0.10234 1.77520 0.07717

## log10(income) 0.87659 0.03506 25.00502 0.00000

summary.rq(f1, se="boot", bsmethod="pwy", R=1000)

##

## Call: rq(formula = log10(foodexp) ~ log10(income), tau = 0.5, data = engel)

##

## tau: [1] 0.5

##

## Coefficients:

## Value Std. Error t value Pr(>|t|)

## (Intercept) 0.18168 0.10261 1.77048 0.07796

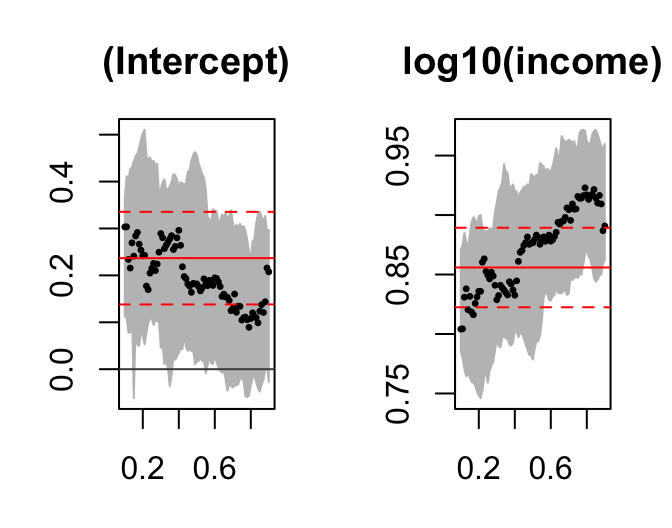

## log10(income) 0.87659 0.03524 24.87675 0.000005.8 Pointwise confidence intervals

tau.seq=seq(0.1,0.9,0.01)

f2 = rq(log10(foodexp) ~ log10(income),tau=tau.seq,data=engel)

sfm = summary(f2, se="rank", alpha=0.05)

plot(sfm, mfrow=c(1,2))